If you're responsible for HR, finance, or workforce systems, this situation is probably familiar. A department head wants to bring in more contractors. Finance wants clean records. IT wants secure processes inside Microsoft 365. Then someone asks a deceptively simple question: what counts as self employed taxable income, and who needs to keep track of what?

That question matters more than many organisations realise. Contractor tax isn't just the contractor's problem. It affects onboarding, expense capture, payment records, audit trails, and the quality of data moving through your HR and finance processes. If the records are patchy, the tax position becomes patchy too.

An Essential Guide for Managing Contractor Tax Compliance

A common scenario goes like this. An HR Director signs off a flexible resourcing model because the business needs specialist skills quickly. Some contractors invoice monthly. Some work on short projects. A few also have part-time employment elsewhere. By the time year end approaches, nobody is fully confident that the right records exist in the right place.

This is why self employed taxable income deserves board-level attention in any organisation using a mixed workforce. In the UK tax year 2022 to 2023, there were 5.63 million self-employment income sources generating £118 billion in total profit, and for those with self-employment income of £5,000 or more, it formed the largest income type at 38% to 89% of total income, according to HMRC’s personal incomes commentary.

For an HR leader, that tells you something important. Many contractors aren't treating self-employment as a small side issue. It's often their main taxable income, which means the data your organisation creates, contracts, invoices, timesheets, approved expenses, and engagement history, can become part of a much wider compliance picture.

Practical rule: If a contractor relationship creates payments, approvals, or reimbursable costs, treat the data trail as part of tax governance, not just supplier administration.

That doesn't mean HR should calculate each contractor's tax bill. It does mean HR and IT should help create a reliable operating environment. A well-structured contractor management system can make that easier by keeping engagement records, approvals, and supporting documents organised from the start.

Understanding Self Employed Taxable Income

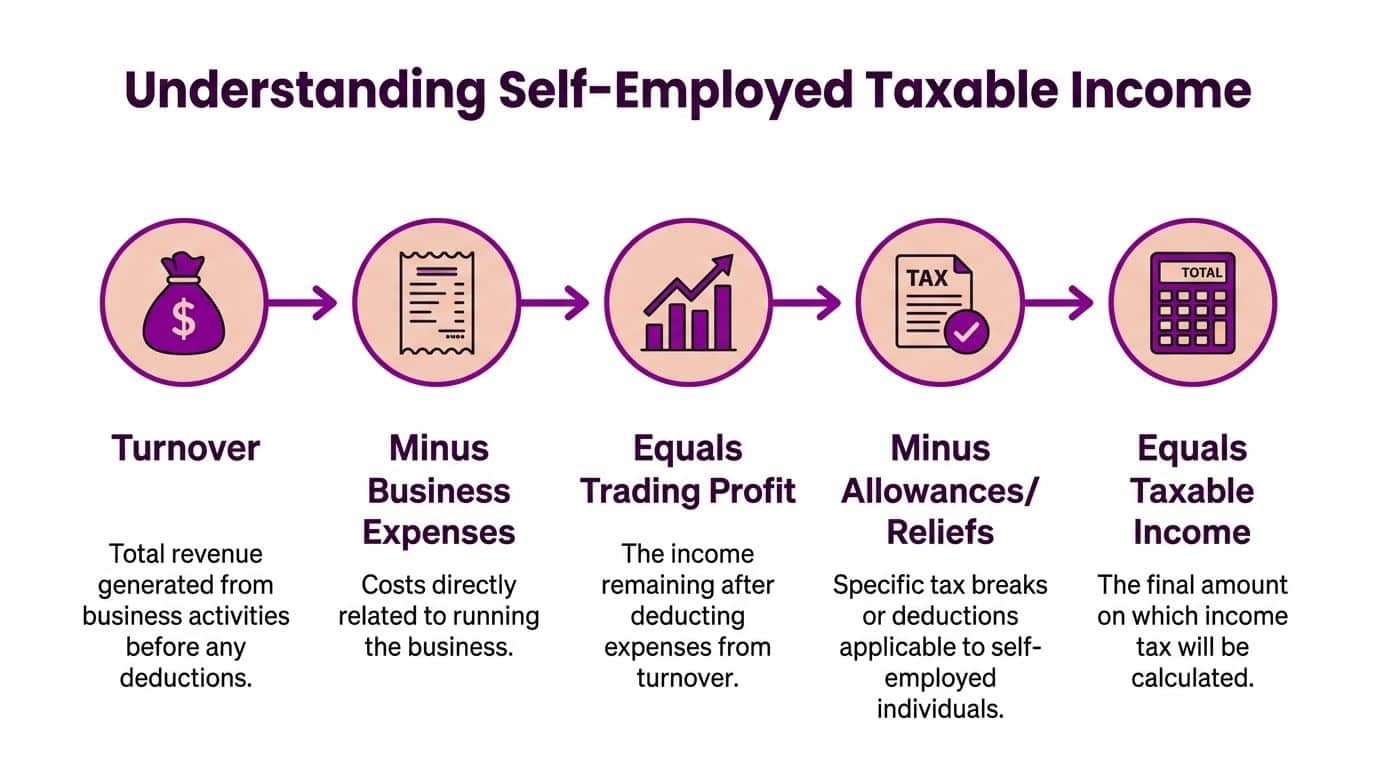

At its core, self employed taxable income is not the money a person receives into their bank account. It's the amount left after working through a sequence of tax steps.

Most confusion starts with one mistake. People mix up turnover with profit.

Turnover isn't the taxable figure

Turnover is the total income from business activity before deductions. If a contractor invoices clients for project work, consulting, or freelance services, that full amount is turnover.

Tax isn't charged on that headline number alone. The tax system looks at what remains after allowable business costs have been deducted. That's why a contractor who invoices heavily during a busy period may still have a much lower taxable amount once genuine business costs are accounted for.

A simple way to explain it to non-finance colleagues is to compare it with a shop. The cash taken at the till isn't the owner's taxable profit. The shop still has to pay for stock, software, utilities, and other business costs before arriving at the profit figure.

The basic flow

In plain language, the process works like this:

- Start with turnover. Add up income from self-employed work.

- Deduct allowable business expenses. These are costs incurred wholly and exclusively for the trade.

- Arrive at trading profit. This is the operating result of the business activity.

- Apply any relevant allowances or reliefs. These can affect the final amount taxed.

- Reach taxable income. This is the figure used for the tax calculation.

That distinction is why good record keeping matters so much. If income is recorded but expenses are not, the taxable figure can be overstated. If expenses are entered carelessly, the contractor may create avoidable risk.

For readers who want a broader primer on how to maximize tax deductions for independent contractors, that guide is useful as background reading, especially when you're helping non-specialists understand why category-level expense discipline matters.

A contractor's invoice total tells you activity. It doesn't tell you taxable income.

Why HR and systems teams should care

In Microsoft 365 environments, confusion often comes from fragmented records. Contracts might sit in SharePoint, approvals in Outlook, time entries in a separate app, and expenses in spreadsheets. When those records don't line up, it becomes harder for the individual to support their tax position and harder for the business to answer compliance questions cleanly.

That's why understanding self employed taxable income isn't just an accounting topic. It's a data quality topic.

How to Calculate Your Trading Profit

Trading profit is the working figure that sits between business activity and tax. Get this wrong and every later calculation is built on shaky ground.

Start with all business income

Trading profit begins with business income received from the trade. For a sole trader or independent contractor, that usually includes fees charged to clients for services provided.

Examples might include:

- Project fees for implementation or consulting work

- Retainer income paid monthly for ongoing advisory support

- Ad hoc invoices for workshops, reviews, or specialist tasks

- Recharged business costs where those amounts form part of the trade receipts

The key point is completeness. If a contractor works across several clients, platforms, or business units, every relevant business receipt needs to be captured. Gaps create problems later.

For HR Directors, this is where process design matters. If managers can engage contingent workers informally, approve work in email, and pass invoices to finance without a common workflow, the business loses the clean trail that supports downstream compliance.

Deduct allowable business expenses

Once income is identified, the next step is to deduct allowable business expenses. These are costs incurred for the purpose of running the trade.

Common categories often include:

- Software and subscriptions such as bookkeeping tools, collaboration tools, or business applications used for client delivery

- Travel for business purposes where the journey relates to work activity rather than ordinary commuting

- Professional services such as accountancy support or certain legal costs

- Marketing and promotion including website costs or advertising used to win business

- Office running costs where the expense is tied to the business

- Training or reference materials where they support the current trade rather than a wholly new one

Contractors often need careful judgement, not guesswork. Some costs are clearly business-related. Others are mixed-use and need more caution.

If you want a practical companion piece focused specifically on expense categories, UK Sole Trader Tax Deductions Explained is a helpful resource for understanding how everyday costs are typically viewed.

Record the reason for the expense when it happens. Months later, people remember the amount but forget the business purpose.

Why disciplined tracking matters

Historical earnings data shows how unstable self-employment can be. Median annual self-employment income declined from £14,535 in 2007/08 to £10,800 in 2013/14, according to the UK government analysis of self-employed income. That kind of volatility is exactly why accurate expense and loss tracking matters.

When income varies from year to year, a contractor can't rely on memory. They need records that show what they earned, what they spent, and what result the business made. For businesses engaging contractors, clean and timely records also reduce friction when finance teams reconcile invoices and supporting evidence.

Capital items and longer-term assets

Some purchases don't fit neatly into day-to-day expenses. If a contractor buys equipment or another longer-term asset for business use, the treatment may differ from ordinary running costs.

The important practical point is this. Don't assume every purchase is deducted in the same way. Larger items often need separate consideration, and the business purpose should be documented clearly at the point of purchase.

A sensible operating approach includes:

- Capture the invoice in a structured digital record.

- Tag the item type so finance can review whether it's an ordinary expense or something needing different treatment.

- Keep approval evidence to show why the purchase was made for the trade.

- Store documents centrally so they can be retrieved later without hunting through inboxes.

In a Microsoft environment, that usually means replacing ad hoc spreadsheets with a more controlled process. An expense management software approach for UK organisations can help standardise categories, approval flows, and document capture so records are easier to support.

What about losses

Not every trading period produces a profit. Some contractors have heavy setup costs, delayed client payments, or uneven project flow. In those cases, loss tracking becomes just as important as profit tracking.

Losses shouldn't be treated as an afterthought. If the records are weak, the contractor may struggle to evidence what happened. If the records are strong, they have a clearer basis for discussing the treatment with their adviser and understanding the effect on future tax outcomes.

A practical calculation example

Suppose a contractor has the following in a tax year:

| Item | Treatment |

|---|---|

| Client invoices received | Added to turnover |

| Business software subscriptions | Deducted if allowable |

| Professional indemnity insurance | Deducted if allowable |

| Business travel to client sites | Deducted if allowable |

| Laptop bought for business use | Reviewed separately from routine running costs |

That process doesn't yet produce the final tax bill. It produces the trading profit. That's the number the tax calculation starts from.

Calculating Your Final Tax and National Insurance Bill

Once trading profit has been established, the government calculation begins. This stage applies the tax bands and National Insurance rules.

For the 2025/26 UK tax year, the PwC UK tax summary states that self-employed income tax is charged at 20% on £12,571 to £50,270, 40% on £50,271 to £125,140, and 45% above £125,140. It also notes that Class 4 National Insurance Contributions are 6% on profits between £12,570 and £50,270, and that Class 2 NICs were abolished from April 2024.

The rates at a glance

| Type | Threshold / Band | Rate |

|---|---|---|

| Personal allowance | Up to £12,570 | 0% |

| Income tax basic rate | £12,571 to £50,270 | 20% |

| Income tax higher rate | £50,271 to £125,140 | 40% |

| Income tax additional rate | Above £125,140 | 45% |

| Class 4 NIC | £12,570 to £50,270 | 6% |

| Class 4 NIC | Above £50,270 | 2% |

| Class 2 NIC | From April 2024 | Abolished |

Worked example using £60,000 profit

Let's use the example provided in the verified data.

A self-employed individual has £60,000 of profit.

First, deduct the £12,570 personal allowance. That leaves £47,430 taxable for income tax purposes.

Income tax is then charged at 20% on that £47,430, which gives £9,486.

Class 4 National Insurance is charged at 6% on £37,700, which gives £2,016.

That produces a combined liability of £11,502.

Where people usually get confused

The most common misunderstanding is thinking the whole profit is taxed at one rate. That's not how the system works. Tax bands apply progressively.

Another confusion point is National Insurance. Some people still expect Class 2 to appear because it existed historically. For current planning, you need to work from the updated rules rather than old habits or outdated articles.

Check whether you're discussing turnover, trading profit, taxable income, or final liability. Those four figures are related, but they aren't interchangeable.

Why this matters for contractor governance

An HR Director doesn't need to prepare each contractor's Self Assessment return. But understanding the shape of the calculation helps when discussing pay rates, expense policies, and contractor communications.

For example, two contractors with the same invoice value can have very different final tax outcomes depending on their allowable costs, mixed income position, and record quality. That's why broad assumptions based on gross payments are usually unreliable.

Digital Record Keeping and The Future of MTD

Tax compliance increasingly depends on digital discipline. Paper receipts, scattered PDFs, and email-only approvals create friction for everyone involved.

What good records look like

At a minimum, a contractor should keep the documents that support income and expense entries. In practice, that usually means invoices issued, supplier receipts, bank evidence, and records showing the business purpose of costs claimed.

For organisations that engage large numbers of contingent workers, the internal side matters too. Statements of work, approvals, onboarding records, timesheets, and reimbursement evidence all help build the context around payments and working arrangements.

A practical digital record set often includes:

- Income evidence such as invoices and remittance details

- Expense evidence including receipts, PDFs, and approval history

- Contract records showing scope, dates, and commercial terms

- Identity and compliance records where relevant to onboarding

- Structured reporting data so information can be reviewed without manual rework

The shift to MTD

From April 2026, self-employed individuals with gross income over £50,000 must comply with Making Tax Digital for Income Tax, including quarterly digital submissions via compatible software, according to Hiscox’s guide to self-employed tax. The same source says automated expense claims may deliver 10% to 15% tax savings where users capture allowable costs more consistently.

That changes the rhythm of compliance. Instead of treating tax as an annual scramble, many self-employed people will need a more continuous reporting habit.

Why this matters inside Microsoft 365

For businesses running on Microsoft 365, MTD shouldn't be viewed as a tax-only issue. It's also a systems issue.

If contractor data sits across Outlook, Excel, SharePoint, Teams, Power Apps, and finance tools without a common model, quarterly reporting pressure exposes every weak point. Duplicate records increase. Supporting documents go missing. Managers approve costs informally. Finance spends time chasing context instead of validating data.

By contrast, a Dataverse-based operating model gives organisations a cleaner foundation. Records can be structured once, approvals can be tracked in workflow, documents can be held in linked repositories, and Power BI can surface exceptions early.

Quarterly digital reporting rewards teams that capture evidence as part of everyday operations, not as a year-end rescue exercise.

What HR and IT should do now

MTD is close enough that waiting is risky for organisations with substantial contractor populations. The sensible approach is to review the process before the reporting obligation arrives.

Focus on a few questions:

- Where is contractor income-related data stored today

- Who approves expenses and how is that approval evidenced

- Can records be linked to the engagement, not just to an email chain

- Can finance extract the right data without rebuilding it manually

- Are line managers following a standard workflow or inventing their own

The businesses that handle MTD well will usually be the ones that solved their data structure problem first.

Navigating Common Self Employment Tax Scenarios

The world is rarely tidy. Many people don't have a single clean stream of self-employed income. They have mixed income, deductions under special schemes, or several sources that sit side by side.

That complexity isn't niche. The verified data states that 4.3 million self-employed people filed Self Assessment in 2023/24, with 1.2 million earning under £10,000, often from side hustles, and that the shift to MTD will increase visibility on this income, according to the linked reference in the brief, Federal Reserve working paper URL as provided.

When someone has PAYE and self-employment income

This is one of the most common points of confusion. A person may have a regular job taxed through PAYE and also freelance in evenings or weekends.

In that case, the tax system looks at the person's total position. The personal allowance and tax bands don't belong separately to each income stream. One stream can use up part or all of the allowance, which changes how the self-employed element is taxed.

For HR teams, this matters because some contractors engaged on a light-touch basis may still have tax complexity well beyond the invoice your business sees.

CIS deductions

Construction Industry Scheme treatment often causes anxiety because money may already have been deducted before the contractor receives payment.

The important principle is that a deduction under CIS isn't the final tax answer on its own. It needs to be reconciled properly through the individual's tax reporting so the overall liability reflects the full position.

Property income isn't the same as trading income

Another frequent mix-up occurs when someone has self-employment and rental income. Both can affect the wider tax calculation, but they aren't the same thing and shouldn't be bundled together casually.

This distinction matters for record keeping. Each income type needs its own supporting records and its own logic. If they are merged badly in spreadsheets or email threads, errors become much more likely.

Cash basis or accruals basis

Some self-employed people account on a cash basis, while others use accruals. The difference is about timing.

- Cash basis records income when received and expenses when paid.

- Accruals basis matches income and costs to the period they relate to.

Neither method should be adopted casually. The right choice affects how the tax picture appears across periods, especially where invoices are raised near the year end or client payment patterns are uneven.

Why workforce context matters

Businesses using a blended workforce often underestimate how varied contractor arrangements can be. A contingent worker may have another employer, a side business, CIS deductions, or property income.

That's one reason it helps to understand the wider contingent workforce model rather than treating every non-payroll worker as if they fit the same pattern.

Key Takeaways for Freelancers and HR Teams

The central principle is simple. Self employed taxable income is built from profit, not turnover. Everything depends on the quality of the records used to reach that figure.

For freelancers and contractors, the priorities are practical:

- Separate business and personal records so income and costs don't blur together.

- Capture expense evidence immediately rather than trying to recreate it later.

- Track the business purpose of costs, not just the amount.

- Use digital tools consistently so quarterly reporting doesn't become a scramble.

- Review mixed income carefully if there's PAYE, CIS, or property income in the background.

For HR, IT, and finance teams, the message is broader. Contractor tax compliance sits partly outside your direct responsibility, but the systems and processes you design have a direct impact on how easy it is for contractors and internal teams to maintain accurate records.

That means cleaner onboarding, structured approvals, well-controlled document storage, and better integration across Microsoft 365. It also means recognising that contractor governance is no longer just a procurement or payroll side issue. It's part of workforce design.

DynamicsHub. Experience HR transformation built around your business. Hubdrive’s HR Management for Microsoft Dynamics 365 is the premier hire-to-retire solution, more powerful, more flexible, and more future-ready than Microsoft Dynamics 365 HR.

Frequently Asked Questions About Self Employment Tax

Is turnover the same as taxable income

No. Turnover is the total business income before deductions. Taxable income is reached only after allowable expenses have been deducted and the relevant tax rules have been applied.

Can self-employed people claim working from home costs

They may be able to claim costs that are connected to business use, but the treatment depends on the facts and on how those costs are calculated and evidenced. The key issue is whether the expense is properly attributable to the trade.

What happens if records are poor

Poor records make it harder to support expenses, reconcile income, and complete tax reporting accurately. Under MTD, weak record keeping is likely to become more visible because reporting becomes more frequent and more digital.

Does having a side hustle still matter if the income is small

Yes. Side income still needs to be considered properly. This is especially important where someone also has employment income, because the interaction between those income streams can affect the final tax position.

Do HR teams need to calculate contractor tax

No, not usually. But HR teams should make sure their engagement, approval, and document processes produce reliable records. That supports compliance, reduces disputes, and helps finance and contractors work from the same factual base.

DynamicsHub helps UK organisations bring HR, contractor processes, compliance records, and Microsoft 365 data into one joined-up operating model. If you're reviewing contractor governance, digital record keeping, or workforce processes around Hubdrive’s HR Management for Microsoft Dynamics 365, visit DynamicsHub. Phone 01522 508096 today, or send us a message.